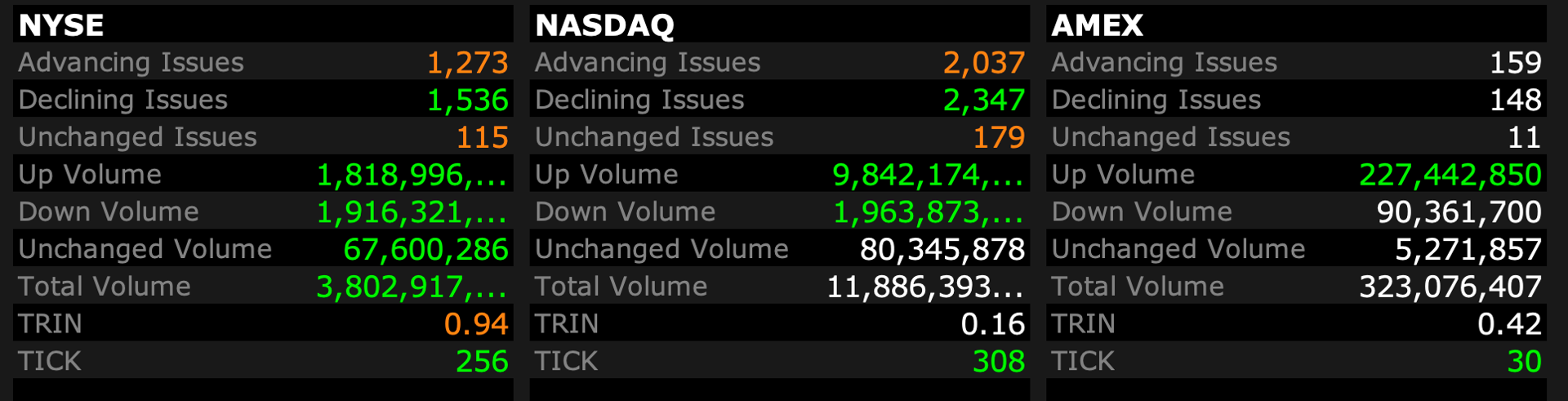

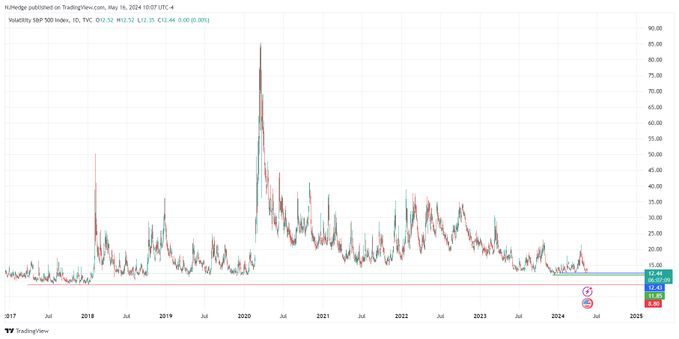

It might be somethin' (resistance/liquidation) or it might be nothin' (normal profit-taking after a sensational move to the upside in a brief period of time) — but the Nasdaq closed with slight negative breadth on extraordinarly high volume.

Not surprisingly no one in the business media has picked up on this:

- NYSE volume 398M shares, 10% below its one-month average;

- NASDAQ volume 10.1B shares, 140% above its one-month average

Teddy... thanks for everything. It has been a pleasure working with you over the years. Your work ethic is amazing and you are among the highest quality people I have worked alongside.

Besides normal profit taking (note how overbought the Oscillator is in an earlier column) - a reversal in bond prices (higher) might be the cause for the selloff from the morning highs.

Here are some yield updates:

* The yield on the 2 year Treasury note is +6 basis points to 4.795%.

* The yield on the 10 year Treasury note is +2 basis points to 4.379%. That is the high of the day and +6 bps from the low yield in the morning.

* The yield on the long bond is only +1 basis point to 4.52%.

I think it was the Dalai Lama who said that "the analysis of death is not for the sake of becoming fearful but to appreciate this precious lifetime."

With ever greater frequency I have experienced another friend's death this week.

The passing of some of the widely recognized people who were part of my business career have been chronicled in my Diary - Ira Harris, Joe Rosenberg and Byron Wien are among those that I have written about.

But with every note of this kind in my Diary, I am reminded of how fortunate I am and that sometimes it is the loss of life that reminds me of how precious life is.

Please give me the next hour or so to recover from the latest loss.

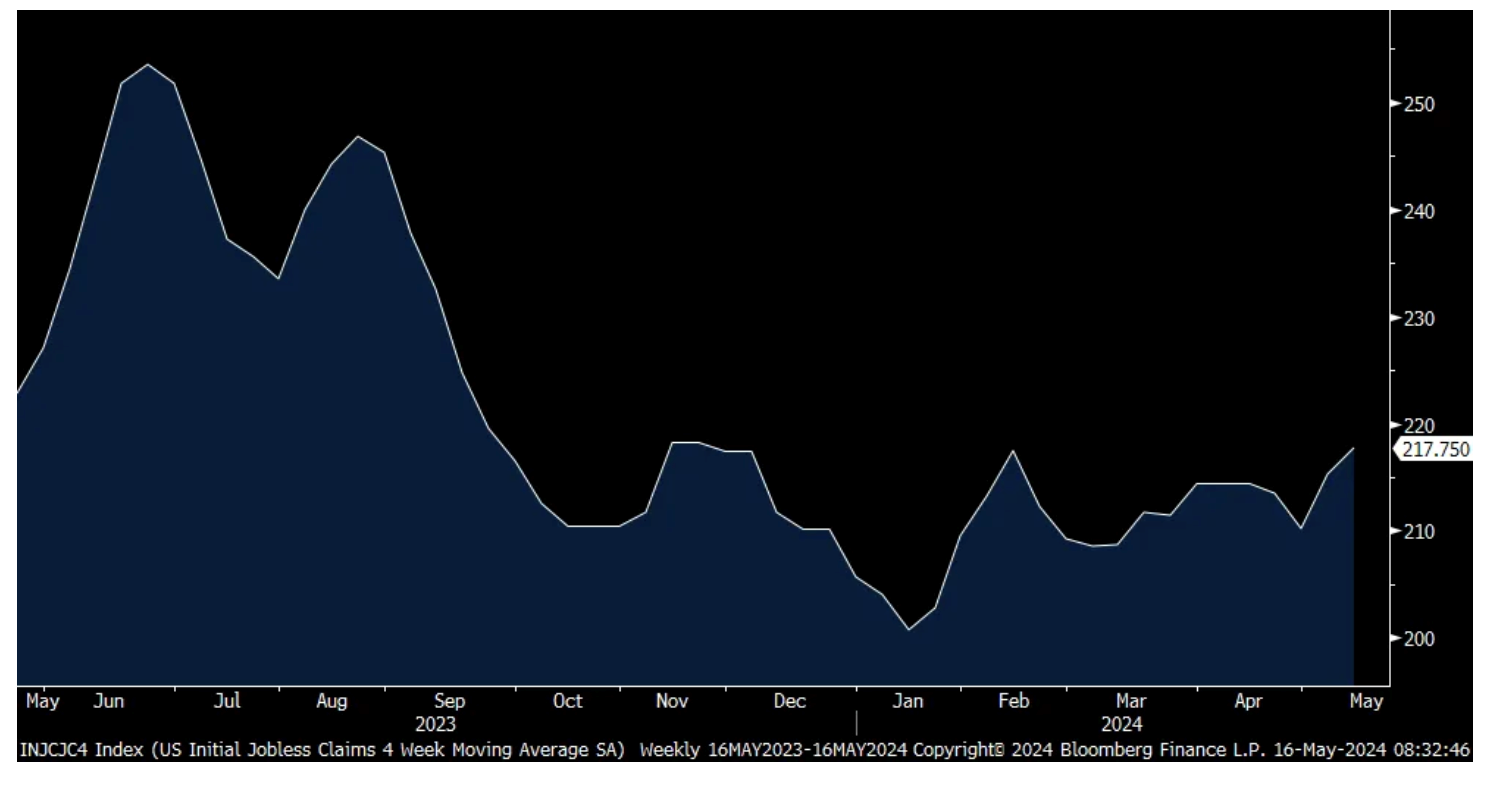

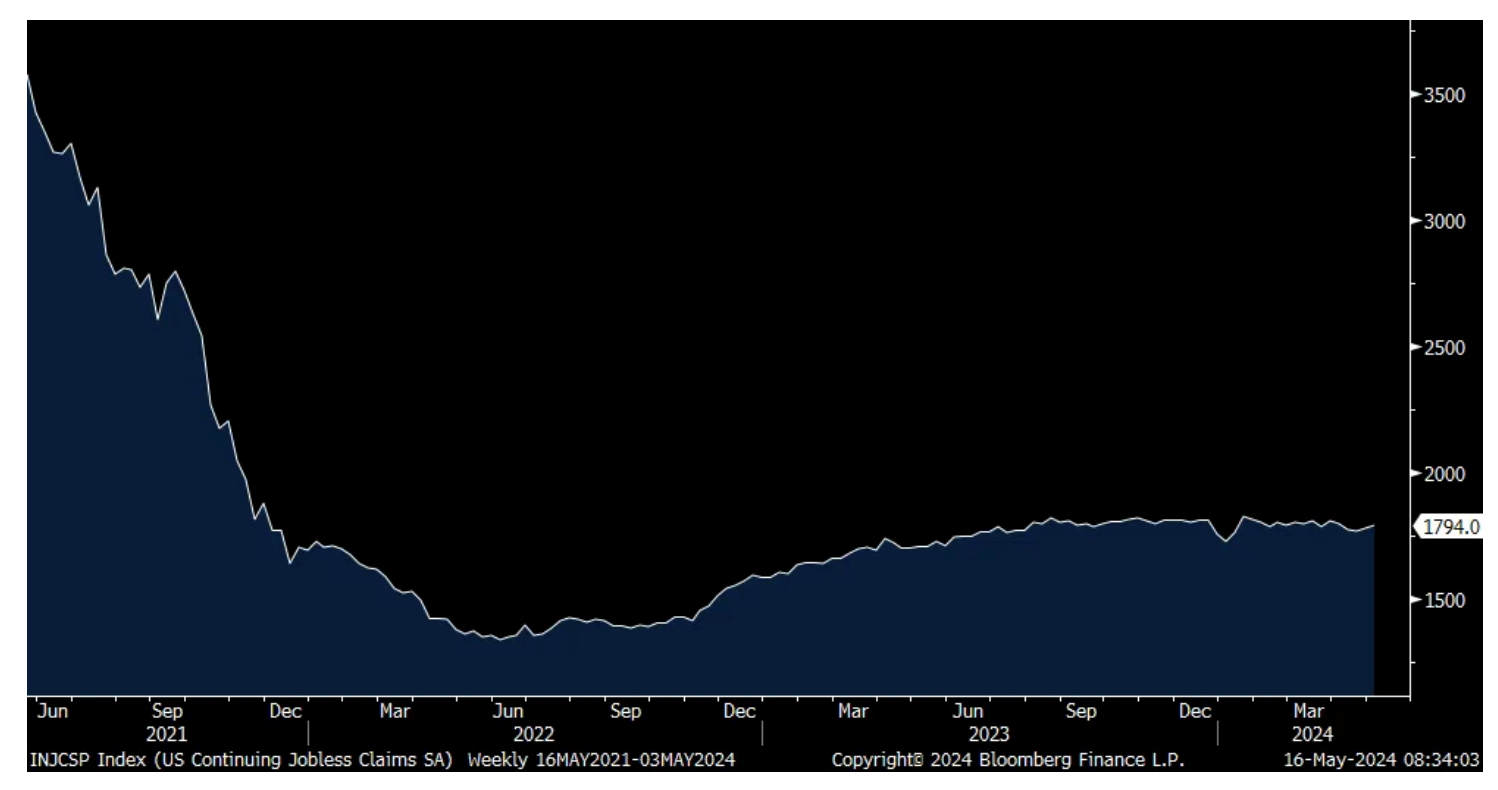

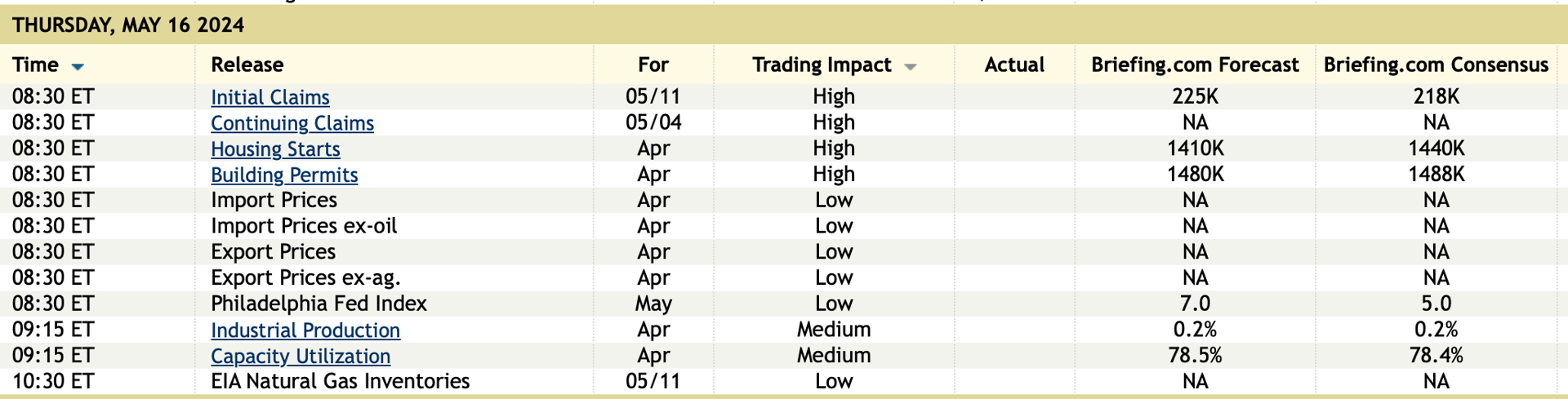

After the upside surprise seen last week in initial jobless claims (partly due to a bad seasonal adjustment on some NY public employees who can claim unemployment benefits during spring break but which they do every year), they remained elevated compared to the recent low trend for the week ended May 11th at 222k, 2k more than expected and vs 232k in the week before.

Smoothing this out has the 4 week average ticking up to 218k from 215k and that is the most since November 2023. Also of note, and not subject to the NY quirk last week, continuing claims rose to 1.794mm from 1.781mm, remaining near the highest since November 2021.

Bottom line, initial claims remain low but we just printed the 2 highest reads in a row since late January so let's keep a watch while continuing claims remain elevated.

4 week avg Initial Jobless Claims

Continuing Claims

While markets breathed a sigh of relief that CPI was about in line, import prices in April far exceeded expectations with a headline jump of .9% m/o/m, triple the estimate and March was revised up to a .6% gain from .4% initially. Also, ex petro saw import prices rise by .7% m/o/m, well more than the forecast of up .1%. Price spikes were seen in food/beverage and industrial supplies but were muted for capital goods, autos/parts and consumer goods.

Bottom line, something to watch but y/o/y prices are still benign, up 1.1% headline, up .7% ex petro, and up .4% ex food/fuels.

After a deeply negative NY manufacturing print for May, the Philly region said its manufacturing index was +4.5 vs +15.5 in April and that, while still positive, was below the estimate of +7.8. New orders fell back below zero for the 1st time since February at -7.9 while backlogs dropped more than 12 pts to -11.5. Inventories remained well under zero at -10.1.

The employment component stayed below zero too and hasn't been above since last October. The workweek too was negative at -8.3. Prices paid fell 4.3 pts to 18.7 but jumped by 20 pts in April. Prices paid rose 1.1 pts m/o/m to a 5 month high, though is around the 6 month average.

Confidence still remains that things will get better in the coming 6 months as the outlook held high at 32.4, though down 1.9 pts m/o/m. The optimism is based on hopes for inventory restocking as this category was positive for a 3rd month. Capital spending plans were little changed.

Bottom line, US manufacturing as seen by the NY and Philly regions is off to another sluggish start in May.

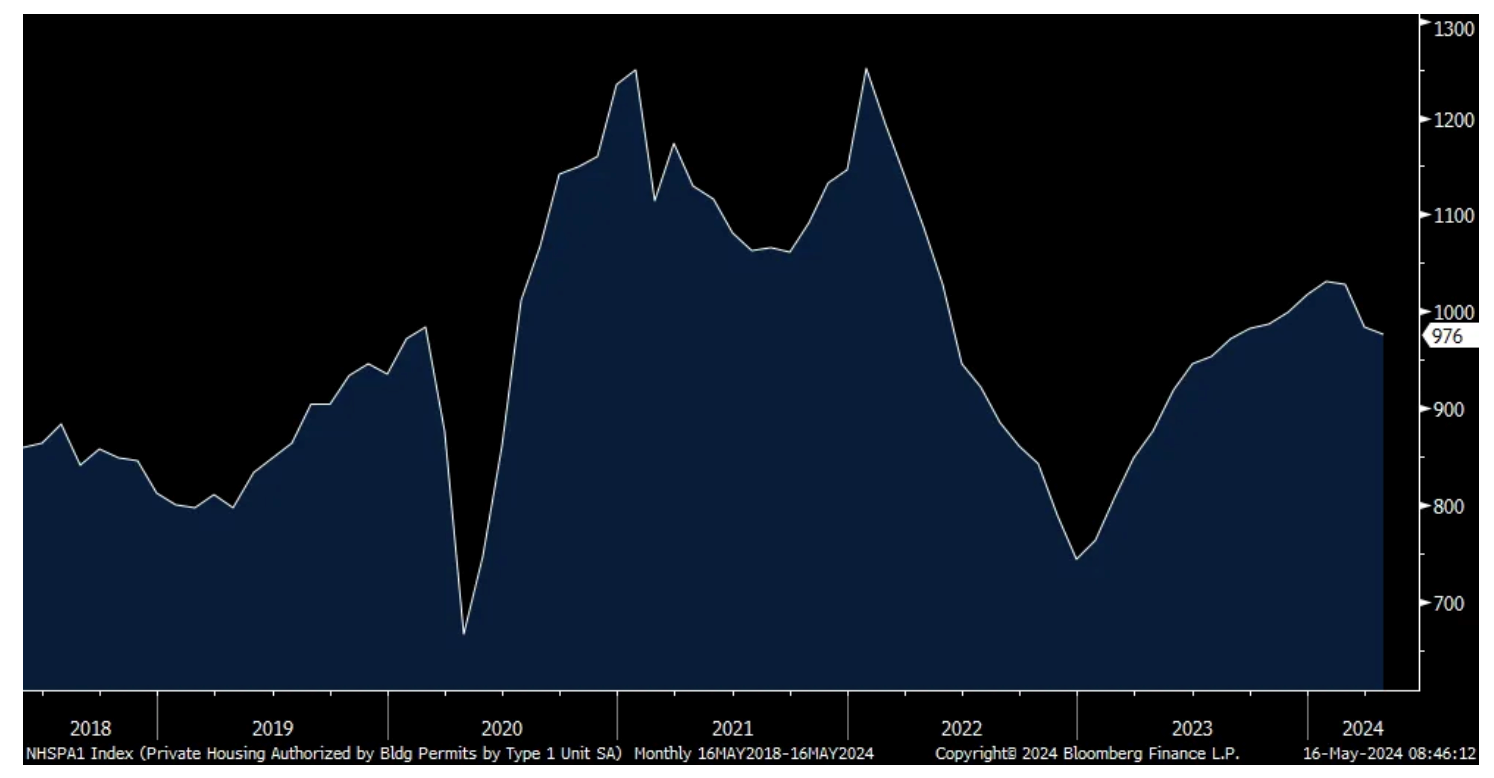

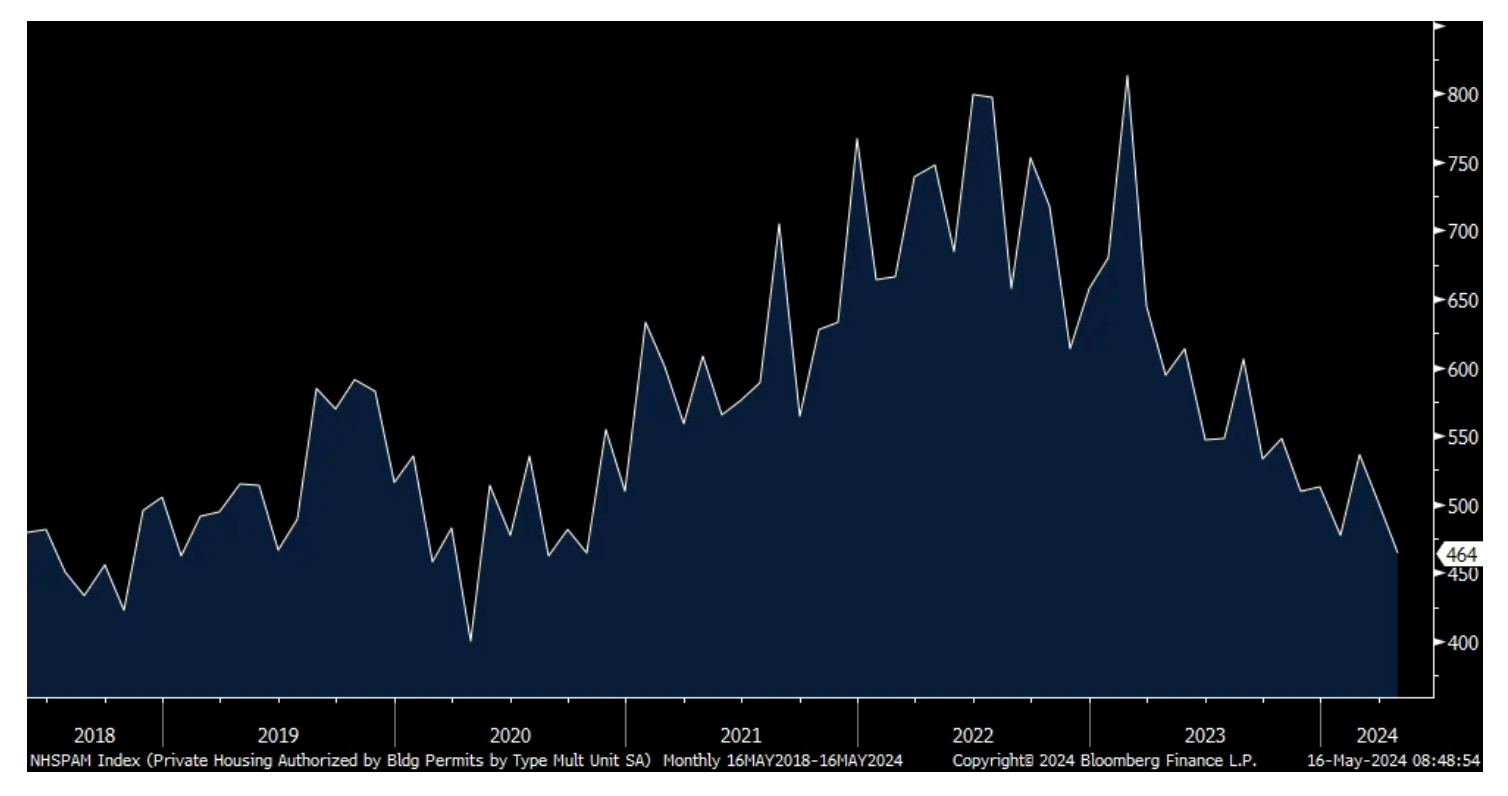

Housing starts in April totaled 1.36mm, well below the estimate of 1.421mm and March was revised down by 34k to 1.287mm. Single family starts held steady at 1.031mm m/o/m while they rose a bit for multi family to 329 after collapsing to just 252k in March and vs 412k in February.

As for permits, they fell 8k m/o/m for single family to 976k which happens to be the smallest since last August. Permits to build multi family dropped by 37k m/o/m to 464k which matches the lowest since August 2020 and the lowest since January 2019 not including Covid.

Again, we have a large amount of multi family supply getting completed this year, green lit a few years ago when rates were low, but once done, there is going to be very little new supply thereafter.

As we look at the future, our teams are focused in the area of cardiometabolic. We have programs internally beyond MK-6024, and we do look externally at the field and the opportunity to see what we can do to bring advancements to patient care.

As we think about obesity specifically, we do think there's the possibility for second and third waves of innovation, maybe with oral agents, agents that have more tolerability, maybe combination products, and maybe products that will have weight loss that is more fat loss, not muscle loss, and it's an area we're focused on.

So as a company, we look to build our strengths, and we will look to invest internally while we'll also evaluate the external landscape.

I may not always love you But long as there are stars above you You never need to doubt it I'll make you so sure about it, God only knows what I'd be without you

God Only Knows might have been the most beautiful song Brian Wilson ever wrote and Carl Wilson ever sung.

The song was on the "Pet Sounds" album, released today 58 years ago - it was The Beach Boys' eleventh album.

The album incorporated classical, pop and jazz music and Wilson's Wall of Sound based orchestrations mixed conventional rock set ups with elaborate layers of harmonies, sounds and instruments rarely seen in rock (bicycle bells, French horns, flutes and even soda cans). "Pet Sounds" revolutionized music production and was ranked #2 in Rolling Stones' "The 500 Greatest Albums of All Time."

As to the markets I respect the overall price momentum - Asian celebrated overnight though Europe did not - but believe that market participants are incorrectly gauging the improvement in price inflation - which seems to be the narrative of bulls.

As to the markets I respect the overall price momentum (Asian celebrated over night though Europe did not) but believe that market participants are incorrectly gauging the improvement in price inflation - which seems to be the narrative of bulls:

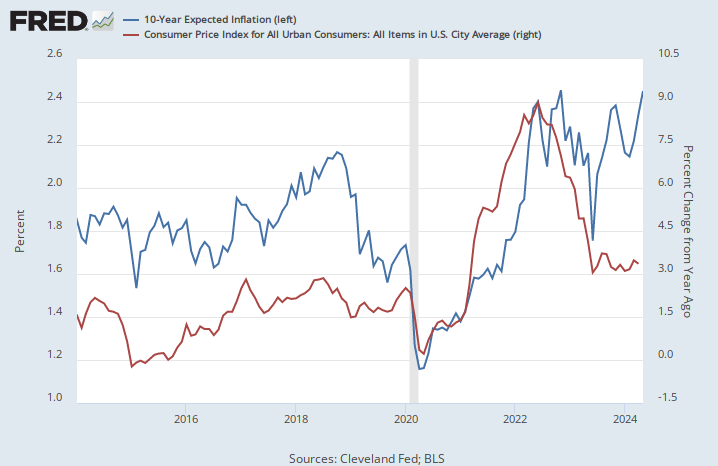

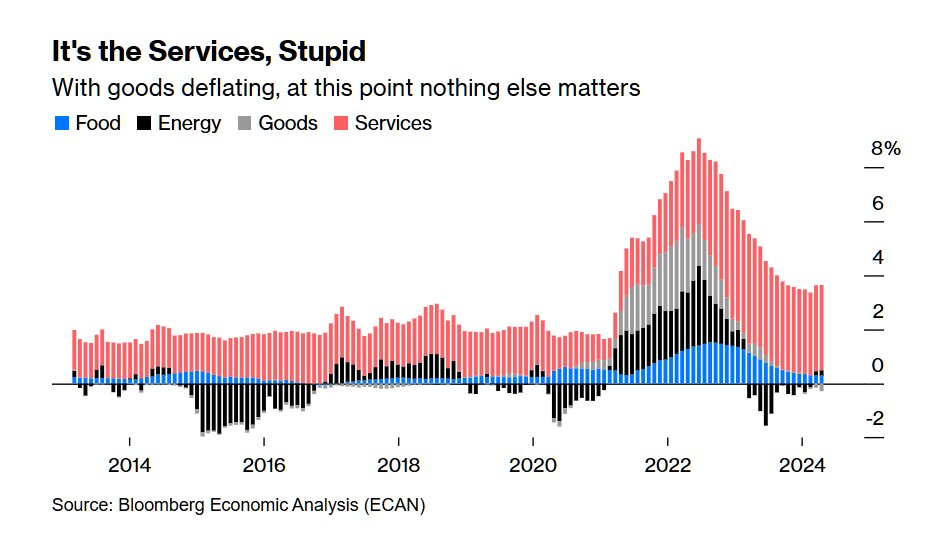

The April CPI report is likely to be the start of a downward trend that takes monthly inflation readings to around 2.5% over the summer. Core-CPI inflation fell from 4.3% in March (m/m, annualized) to 3.5% in April. Our optimism, however, is far more about the economic forces driving inflation than a single reading that, while better, is still elevated. The productivity slowdown (growth fell from 3.5% in 4Q2023 to 0.3% in 1Q2024) that caused higher inflation this year is over. Inflationary expectations, especially for businesses, are subdued. Monetary policy remains tight. Finally, although April producer-inflation was hot with core-PPI coming in at 5.9% annualized, core-PPI is at just 2.4% y/y. There is no economic mechanism that would cause a sustained resurgence in inflation.

April inflation was driven by the usual suspects, especially shelter and transportation services, which make up 45% and 8% of core-CPI. We have long advocated for removing shelter from CPI to obtain “supercore” inflation. This measure fell from 3.7% to 2.6% in April and is at just 2.0% y/y. We like the supercore measure not just because shelter inflation is badly measured; one-third of core-CPI is owner equivalent rent (OER), which just asks homeowners how much they would expect to pay in rent. Just as importantly, core-PCE inflation, the Fed’s preferred measure, puts far less weight on OER. Figure 1 shows that since 2022, core-PCE has been about halfway between core-CPI and supercore, suggesting an April core-PCE reading around 3.1%.

Figure 1: Core-CPI, Core-PCE, and Core-CPI, ex-shelter Inflation (y/y)

There will be no immediate change in the Fed’s tune about wanting to see more progress on lower inflation before cutting rates. To start cutting, the Fed will need even better reports in coming months, which we expect, and more signs of mediocre growth which, as we discuss below, continue to mount. We still expect the Fed to start cutting in July, with additional 25 bps rate cuts in November and February 2025, with the Federal Funds rate falling to 275-300 bps by mid-2026.