On Inflation

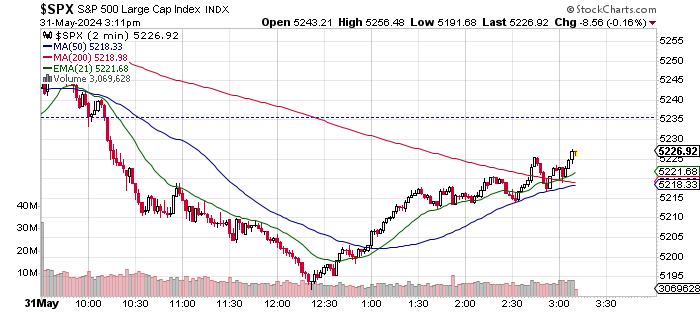

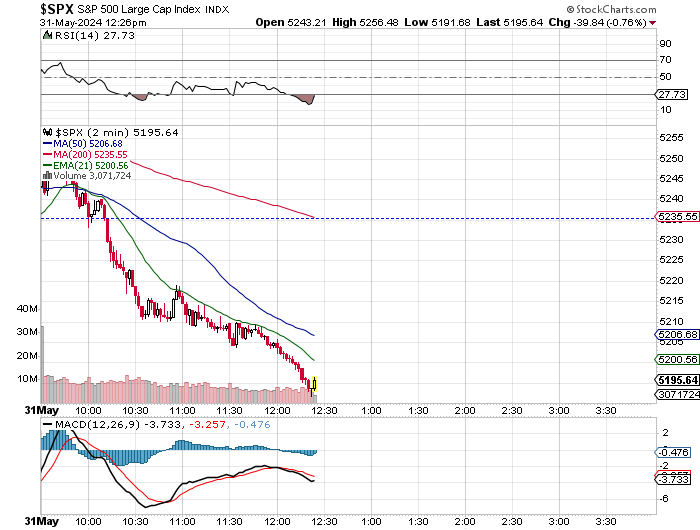

This Friday morning, headline April PCE crossed the tape at month over month growth of 0.3%, maintaining the pace set in February and held steady through March. The year over year print landed at growth of 2.7%, also maintaining the pace set in March. Both of those numbers printed precisely upon consensus view. As mentioned in Market Recon this morning, it's pretty difficult to surprise on PCE given how late in the month the series is released.

That said, core prices did surprise. Just a wee bit, but a surprise to the downside, which is exactly what the policy junkies wanted to see. That's why we experienced an early rally across equities that is quickly giving way to the forces of darkness and selloffs. At the core, April PCE inflation hit the tape at month over month growth of 0.2%, below expectations for 0.3% and down from 0.3% for both February and March, and 0.4% for January. An actual slowing of core price increases? Sounds like it. On a year over year basis, core PCE crossed at growth of 2.8% as expected, and for a third consecutive month.

Hitting the tape alongside the PCE data, Personal Income grew 0.3% in April, down from 0.5% growth in March, while Personal Spending in April increased just 0.2% a month after households were scorched for spending growth of 0.7% in March. This report does not really hurt or help, in my opinion the FOMC gets to a place where a rate cut - or hike - would be considered something that could happen soon.

On GDP

We all saw the Q1 GDP revision, which while reflecting meager growth of 1.3%, was at least somewhat accurate with GDI printing at growth of 1.5%. Readers will recall back in Q3 2023, there was an inescapable mismatch between the two, which is why there was and remains so much doubt about actual economic growth for quarters one through three for calendar year 2023.

Annualized q/q growth for quarters one through three for 2023 averaged growth of 3.07% when measured solely in GDP, but just 0.97% when measured in GDI. Now, keep in mind the huge downward revisions to 2023 job creation data that the Bureau of Labor Statistics has already let us know through their BED report in April are on the way.

By the way, just for the new kids, honest economists in discussing economic growth average GDP and GDI when the two diverge. An adherence to GDP when GDI does not measure up is a telltale sign of either an undereducated economist or more likely in this climate, a politically biased economist.

Atlanta

As mentioned this morning, Thursday's print for April Goods Trade Balance would force the Atlanta Fed to rein in its GDPNow model for Q2. That's exactly what happened this morning. Atlanta took that estimate down to growth of 2.7% (q/q, SAAR) from 3.5% as the inputs for real net exports, and real personal expenditures were decreased, and the input for real gross private investment was increased, slightly offsetting the downward impact of the prior two mentions.

This also means that the New York Fed and St. Louis Fed will likely revise their models lower this weekend as well. New York stood at growth of 2.04%, while St. Louis stood at growth of 1.42%. Both revise their models weekly unlike Atlanta which does so almost in real-time. Cleveland also runs a model that is more the result of its interpretation of the slope of the yield curve and not based on incoming macroeconomic data.