From Peter Boockvar:

Succinct Summation of the Week’s Events:

Positives,

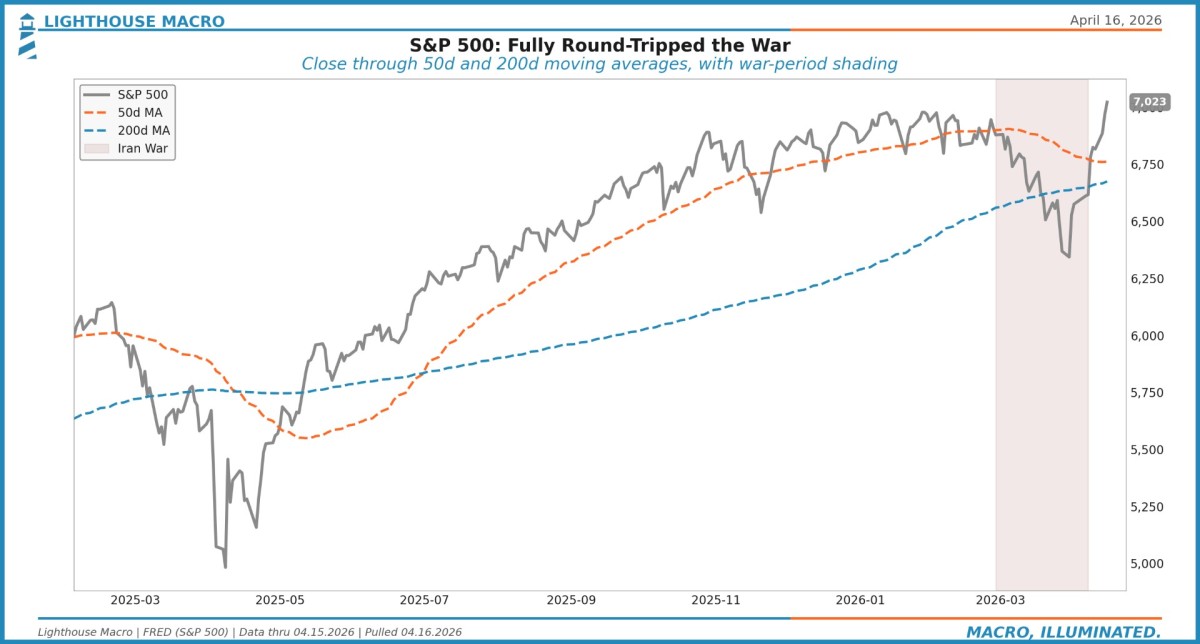

1) The ceasefire is holding, we seem to be close to a deal and the Strait is reopened during the ceasefire according to the Iranian Foreign Minister.

2) Initial jobless claims for the week ended 4/11 fell to 207k from 218k but the 4 week average was 210k vs 209k last week because a print of 205k fell out from 5 weeks ago. Continuing claims lifted back above 1.8mm at 1.818mm but still remaining below the 1.9mm range which has been the upper end of the range since November 2021.

3) The April NY manufacturing index for April rebounded to +11 from essentially zero at -.2 in March and +7.1 in February. New orders jumped to 19.3 from 6.4.

4) The April Philly index rose to 26.7 from 18.1 and above the estimate of 10. As also seen in the NY survey, new orders jumped to 33 from 8.6 and I continue to believe that we have companies that are front running ordering in order to create extra inventories so as not get caught short on any supply shortages.

5) Container shipping prices according to the World Container Index were down w/o/w with the Shanghai to LA route down 3.4% w/o/w after jumping by 9% last week. Shanghai to NY slipped 3% after a 32% rise over the prior six weeks. The price was also down for the Shanghai to Rotterdam trip.

6) March PPI rose another .5% m/o/m after a .5% jump in February but that was well below the estimate of a 1.1% increase and February was revised down by 2 tenths. The core rate was up just one tenth m/o/m vs the forecast of up .4% and vs a .3% gain in February (downwardly revised by 2 tenths) .

7) After a big jump seen in February of .9% m/o/m (revised down from 1.3%) , March import prices rose another .8%, though that was well below the estimate of 2.3%. The y/o/y gain went to 2.1% from 1.3% and that is the most since December 2024. Import prices ex petro rose just one tenth m/o/m but was up .9% in February, .8% in January and .4% in December and still up 2.6% y/o/y. Taking out both fuels and food saw an import price jump of .6% m/o/m vs .9% in February, .7% in January and .3% in December and higher by 3.5% y/o/y.

8) The average 30 yr mortgage rate fell 9 bps w/o/w to 6.42% and that helped refi’s rebound by 5.1% after big declines in the prior four weeks. Purchases were little changed though, down 1% after rising by a like amount last week.

9) From Pepsi: “We’ve had no major issues from a supply chain standpoint. We’re seeing really nice continuity there. The teams are managing it well. I think in times like these, the scale of PepsiCo is really an advantage.” Also, “We do have some systemic hedging programs in place that does give us some near term visibility here. We typically have about 6-12 month hedges in place. Now, our assumption is that inflation will come. The order of magnitude we’re still working through, and I think a lot of that is still to be determined.” And, “From a visibility and guidance standpoint, our assumptions are that we can mitigate what comes our way this year, and that’s really reflected in our assumptions on guidance.”

10) From Manpower: “Within Talent Solutions, our RPO (recruitment process outsourcing) business continues to experience a sluggish permanent hiring environment, but we did see sequential revenue trend improvement.” On the impact of AI on hiring, “I think it’s basically uncertainty related to the economic environment and outlook. Employers are getting buffeted by geopolitical events, tariffs, wars, that are ongoing or started and that clearly drives employer hesitation. So in our mind, the client hesitation is more related to those events than any particular concerns or possible impact of AI into their workforce.”

11) From JB Hunt: “As we moved through the first quarter, the freight environment felt meaningfully different than what we’ve operated in over the past several years. When we spoke last quarter, I described the truckload market as fragile, and that we are testing the elasticity of supply, and that assessment proved accurate. Continued regulatory enforcement to improve safety in our industry has removed non-compliant capacity, and when combined with early signs of improved demand, resulted in a tighter truckload market throughout the quarter. While predicting inflection points is never precise, we believe we are on a path of recovery.” More on the capacity shrink that continues, “What we’re seeing is a freight market that has fundamentally less slack than it did in prior cycles. Capacity has been steadily exiting for an extended period, driven by regulatory enforcement, rising costs, and financial performance that does not support capital reinvestment...Truckload rates, tender rejections, the ISM PMI, and several others are all at their highest levels since 2022. And trucking employment is at the lowest levels since 2022, all proof points of structural change.”

12) From Taiwan Semi: “In terms of material supply, TSMC’s strategy is to continuously develop multi-source supply solutions to build a well diversified global supplier base and to improve the local supply chain. For specialty chemicals and gases, including helium and hydrogen, we source from multiple suppliers in different regions, and we have prepared safety stock inventory on hand. We are also working closely with our suppliers to further strengthen the resiliency and sustainability of our supply chain. Thus, we do not expect any near term impact on our operations from material supply.”

13) From Bank of America: “Our research team continues to see an economy that is resilient, that the core activities of the economy continue to push along even with all the uncertainty that you’ve all written about out there. We see the forward look of GDP growth rates in the US in the 2% range, and we see a faster growth rate around the world...Turning briefly to asset quality, we saw improvement from last year. Net charge-offs, card delinquencies, reservable criticized assets, and non-performing loans, all declined vs the first quarter of ‘25. Provision expense was $1.3 billion compared to $1.5 billion last year, reflecting continued benign credit results.”

14) From JP Morgan: “Notwithstanding the recent volatility in market and gas prices, based on our data, consumers and small businesses remain resilient, with consumer spend growth continuing above last year’s pace.” In their investment banking and M&A business, “Looking ahead, client engagement and pipelines remain healthy, but of course, developments in the Middle East could have an impact on deal execution and timing.” What are they seeing on the US consumer? “There really is not anything new or interesting to say this quarter. We’ve looked at it through every angle, early roll rates, delinquency rates, cash buffer, spend, discretionary spend, non-discretionary spend, it all looks consistent with prior trends and fundamentally healthy…So think gas or energy costs is something like 3% of the typical consumer’s expense – spend expenditure, at least in our portfolio. So, it’s not nothing, but it’s not overwhelming. We’ve looked to see if there’s kind of evidence in there of people trading, decreasing other discretionary spending to adjust for higher gas prices, but it’s just kind of not enough yet to be visible.”

15) From Wells Fargo: “While the markets have reacted to macroeconomic uncertainty, our actual credit performance in the first quarter remains strong. Our net loan charge-off ratio was stable from a year ago and increased 2 bps from the fourth quarter. Commercial credit continues to perform well, and we are not seeing signs of systemic weakness.” With their consumer loan book, “We continue to closely monitor our portfolios for signs of weakness, but have not observed recent deterioration or meaningful shifts in trends.”

16) China’s economy grew by 5% y/o/y in Q1 vs the estimate of 4.8% with strength in industrial production. Retail sales remain lackluster as the consumer is still managing the decline in residential real estate prices. Though prices are falling at the slowest pace in a year and are now rising m/o/m in Shanghai, Shenzhen and Guangzhou while flat in Beijing vs continued declines in 2nd and 3rd tier cities.

17) The UK economy in February rose .5% m/o/m, well better than the estimate of up .1% with help from services and construction.

Negatives

1) Another week of lost shipments of so many needed things but hopefully no more.

2) Within the Philly manufacturing index, not surprisingly, prices paid jumped to 59.3 from 44.7 and that is the most since last August. Prices received also rose to the highest since August at 33.5 vs 21.2 in the month before. In the NY survey, there was the 14.4 pt jump in prices paid to 51, the highest since last October but those received were little changed, for now, up .4 pts to 21.8.

3) The April NY Fed’s services index for that region remained in contraction at -14 but less so and vs -22.6 in March.

4) Dry bulk shipping prices rose for the 9th straight day by another 5.5% to 2,484, the highest since December according to the Baltic Dry Index.

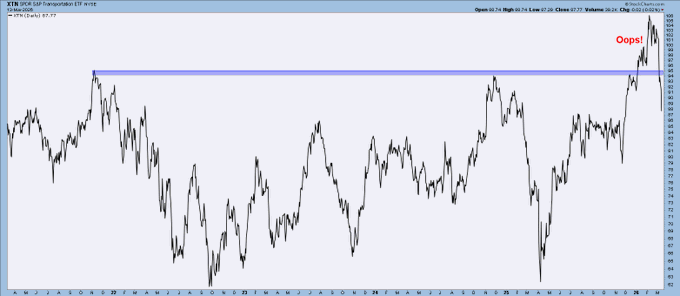

5) The US oil patch is still not responding to higher prices and again, looking at the back end crude oil futures market rather than front month in making drilling decisions. The Baker Hughes crude oil rig count was unchanged w/o/w and up just 4 since the war broke out, still hovering around the lowest level since September 2021.

6) This is how the Fed’s Beige Book summarized the US economy over the past six weeks, “Overall economic activity increased at a slight to modest pace in eight of the twelve Federal Reserve Districts, while two Districts reported little change and two Districts reported slight to modest declines. The conflict in the Middle East was cited as a major source of uncertainty that complicated decision-making around hiring, pricing, and capital investment, with many firms adopting a wait-and-see posture.” Quite the mixed bag.

7) The April mood of homebuilders softened further to 34 from 38 in March. The estimate was 37. The Present Situation fell 4 pts m/o/m to 37 while the Future look was down by 7 pts to 42. Prospective Buyers Traffic is not helping with it down 3 pts to just 22 after rising by 3 pts in March. Higher energy prices have had an immediate impact from a construction perspective. The NAHB said “With oil prices higher in the US, 62% of builders reported suppliers have increased building material costs due to higher fuel prices, including gas and diesel. With near-term economic risks elevated, 70% of builders reported challenges pricing homes given uncertainty about material costs.” As for the demand side and that depressed level of interested buyers, “buyers face ongoing elevated interest rates and growing economic uncertainty. The year started with hopes for housing momentum growth, but risks with respect to the Iran war, energy costs, and declines for consumer confidence have slowed the market.”

8) The NFIB Small Business Optimism index for March fell 3 pts m/o/m to 95.8 and that is the lowest since April 2025. From Bill Dunkelberg at the NFIB, “The 20% Small Business Deduction and other supportive small business tax provisions in the Working Families Tax Cut Act have had many positives for small business owners,” said NFIB Chief Economist Bill Dunkelberg. “However, the dramatic spike in oil prices has spooked consumers and owners alike. Small business owners are having to absorb those higher input costs and pass them along to their customers.”

9) From Knight Swift Transportation: “While the winter weather negatively impacted volumes and operating costs more than typical for a first quarter, it also exposed the reduction in truckload capacity to all stakeholders, which is very meaningful for ongoing bid activity. Similarly, the rapid increase in fuel costs was a headwind to earnings in March, but we believe this will add to the existing downward trend in supply in the truckload industry. The truckload market continues to tighten, and the bid environment is rapidly evolving.”

10) From Alcoa: Broadly with the effective Strait closure, “more than 2.5 million tons of annual smelting capacity and nearly 2 million tons of refining capacity are offline year-to-date. That’s a meaningful disruption to the global system. Alumina refineries in the region are integrated with aluminum smelters. However, approximately half the region’s bauxite requirements are imported from outside the Middle East. This structure leaves the regional aluminum system particularly exposed to shipping disruptions and logistical constraints. And it doesn’t stop at bauxite and alumina. Several smelters in the region also rely on imported anodes, calcined coke, and coal tar pitch. With transit through the Strait restricted, these materials are harder to move, raising costs and increasing uncertainty. Given the Middle East’s important role in global green petroleum coke exports, these disruptions are already rippling through the global calcined coke market...The takeaway is clear. Structural dependencies in the Middle East mean that disruption there doesn’t stay local. It moves quickly through the aluminum value chain, tightening supply, increasing cost volatility and elevating risk well beyond the region itself.”

11) From Fastenal: “Industrial economy remains somewhat challenging with US manufacturing PMI averaging around 52.6, which is an improvement, but still moderate overall. We really didn’t see much of a tailwind. We gained share through focused execution. Largely, we won new business with key accounts, we expanded customer site presence and we strengthened our value added services and solutions.” What disappointed the Street, “We were approximately 40 bps below our own Q1 gross margin target, as pricing actions did not keep up with cost increases as the quarter played out...Tariff related costs moved through the P&L faster than our pricing...On pricing, we realized approximately 3.5% y/o/y and that compares to 3.3% in the fourth quarter, not enough to offset inflation.”

12) From Citigroup: “Switching gears, the global macroeconomy to date has weathered shock after shock. However, the impact of the Middle East conflict is hitting Asia and Europe harder than countries such as the US and Brazil, which are more insulated from energy shocks. Clearly, the longer this goes on, the more pronounced the second and third order impacts are going to be around the world. And inflation is now a greater risk to growth that will likely cause central banks to lean towards more restrictive monetary policies.”

13) From Wells Fargo: “Client sentiment is cautious but engaged as macro and geopolitical uncertainty has increased and clients have largely shifted to a more selective and defensive posture.”

14) From Carmax: “Our EPS during the quarter was impacted by restructuring costs as well as by a non-cash goodwill impairment, while our margins decreased from the prior year quarter as we continue our focus on targeted price reductions and driving sales.” On their auto finance business, “Consistent with the third quarter, credit losses in the fourth quarter were in line with our expectations.” But, “With regard to roll rates and delinquencies, I think across the auto lending industry, lenders would say, customers, maybe absent exception of the highest credit quality, the 800 plus FICO, they certainly are feeling the stress of affordability, inflation, etc...So, those customers from mid-Tier 1 all the way down to deep subprime are feeling the stress, delinquencies are higher, roll rates are higher, and for us as a lender, our job is to support them, help to service them, and then set the reserve accordingly in preparation for that...But there is a stressed customer out there, and we are thoughtful on that.”

15) From Albertson’s: “In grocery, units and ID sales in Q4 remained pressured in our lowest income cohorts. Egg deflation also created a meaningful sales headwind as we cycled the significant egg shortages from a year ago, a dynamic that we expect persist into the first quarter of 2026.”

16) From Kering: Group revenue fell 6%, “impacted by the strengthening of the euro, and stable y/o/y on a comparable basis. This stabilization represents an important first milestone and a further sequential improvement. It was delivered in a challenging and uncertain environment, with low visibility and continued pressure on consumer confidence. Geopolitical tensions, notably in the Middle East, also weighed on traffic and performance during the quarter.”

17) From LVMH: “LVMH continued to grow organically in Q1 with improved trends across most businesses. The quarter was impacted by the ongoing conflict in the Middle East, which had a tangible incidence on demand in the region in March after a good start of the year, and this accounted for a negative 1 percentage point on the growth of the quarter. So, excluding this impact, organic growth would have been plus 2%...Elsewhere, Q1 saw solid growth in China and Asia at large as well as in the United States...The euro strength against key currencies generated a negative 7% currency impact in Q1, which continued to have also an unfavorable impact for tourist sales, especially in Europe.”

18) Lending Tree released an updated analysis on Buy Now, Pay Later and they said this, “A growing percentage of buy now, pay later (BNPL) users say they’ve paid late on one of these loans in the past year. Now, 47% of BNPL users have done so, up six percentage points from 2025 and 13 percentage points from two years ago...That’s just one of the troubling findings...We asked consumers about their behaviors and perspectives regarding these popular loans. Along with increased late payments, we found that more users are buying groceries with these loans and carrying three or more BNPL loans at once, and that more than half of BNPL users say they wouldn’t be able to make ends meet without them.”

19) The March slowdown in global trade was seen in the China trade data where exports were up 2.5% y/o/y, well below the estimate of up 8.6%. Imports jumped by 28% as I’m sure importers were rushing to get things. That’s twice the forecast of a rise of 14%.

None.