Tilray Was Ripe for a Selloff. Is It Now Ripe for a Trade?

Obviously, at some point, one has to think that a short-squeeze might emerge.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Freaking ugly. Less than. I guess.

Tilray Brands TLRY released its third-quarter financial results on Tuesday morning. For the three-month period ended February 29, the company posted a GAAP loss per share of $0.12 on revenue of $188.34M. Though the revenue print is good enough for year-over-year growth of 29.3%, these top and bottom-line results both badly missed expectations.

There is some mixed to good news. Beverage-alcohol net revenue increased 165% to $54.7M from the year-ago period. That increase was largely due to the company's new Craft Acquisition Brands, while existing brands remained consistent. Gross profit for this business increased 89% to $18.9M, as gross margin for that business narrowed to 34% from 48%.

Global cannabis net revenue rose 33% to $63.4M from a year earlier, also reflecting acquisitions as well as growth in Canadian medical usage. Gross profit for cannabis increased to positive $20.9M from the year ago comp of -$32.8M. Cannabis gross margin improved to positive 33% from -69%.

Distribution net revenue decreased 13.2% to $56.8M as Distribution gross margin dropped to 10% from 11%. Wellness revenue increased 12% to $13.4M

Operations

As revenue grew 29.3% to $188.34M, the cost of goods sold decreased 11.7% to $138.9M, leaving a gross profit of $49.4M, up from -$11.7M a year ago. Operating expenses decreased from $1.195B a year ago to $131.5M. For this reason, Tilray's operating loss improved to $82.1M from $1.207B.

It is important to note that for the year-ago period, Tilray recognized $934M in impairments and for the period being reported, it did not post anything along those lines. After accounting for interest, taxes, and non-operating expenses, net loss printed at $104.983M, improving from a loss of $1.196B. This is how we got to a GAAP loss of $0.12 per share, which still stinks, but compares well to -$1.90 a year earlier.

Fundamentals

Fiscal year to date, Tilray has generated operating cash flow of -$61.6M. Tack on Capex spending of $19.5M and that leaves a free cash flow of -$81.1M.

Turning to the balance sheet, the company ended the quarter with a cash position of $146.3M and inventories of $244.1M, putting current assets at $631.2M. (Cash is down 29% fiscal year to date, while current assets are down 18.4%. Inventories are up 18%.) Current liabilities add up to $329.1M.

Though that leaves the company with a current ratio of 1.92 and a quick ratio of 1.18, both of these ratios appear healthy enough. However, it does have $27.4M in short-term debt as well as $83.4M in convertible debentures payable that will all have to be dealt with within a year. Tilray has the cash on hand, so there is no crisis, but there will very likely be a refinancing of a significant portion of that debt load at higher interest rates.

Total assets amount to $4.213B, but that includes $2.94B in goodwill and other intangibles. At 69.8% of total assets, this leaves a frighteningly small portion of assets as actually tangible. Especially for a company that is burning cash. Total liabilities come to $869.8M, including another $165.6M in long-term debt and another $126.6B in convertible debenture eventually payable.

Even with the strong ratios, I would be hesitant to give this balance sheet a passing grade. There's a decent enough amount of hair on this.

Guidance

For the full fiscal year ending May 31, Tilray is now guiding toward an adjusted EBITDA target of $60M to $63M, down from prior guidance of $86M to $78M. Ouch.

The company is also (and this is also a big reason that the shares are trading lower Tuesday morning) no longer expecting to generate positive adjusted free cash flow for the full fiscal year, due to the timing of payments for various assets sold.

Word of Warning

Though the shares are trading lower, almost 16% of the float is held in short positions. Obviously, at some point, one has to think that a short-squeeze might emerge.

My Thoughts

Honestly, I did not see anything outside of the short interest that might provoke in me the urge to get long this name.

On the other side of the token, I don't short $2 stocks and I don't short stocks where more than 8% of the float is already short. That's how you can have your head handed to you. So, I am stuck, unless there is an options play.

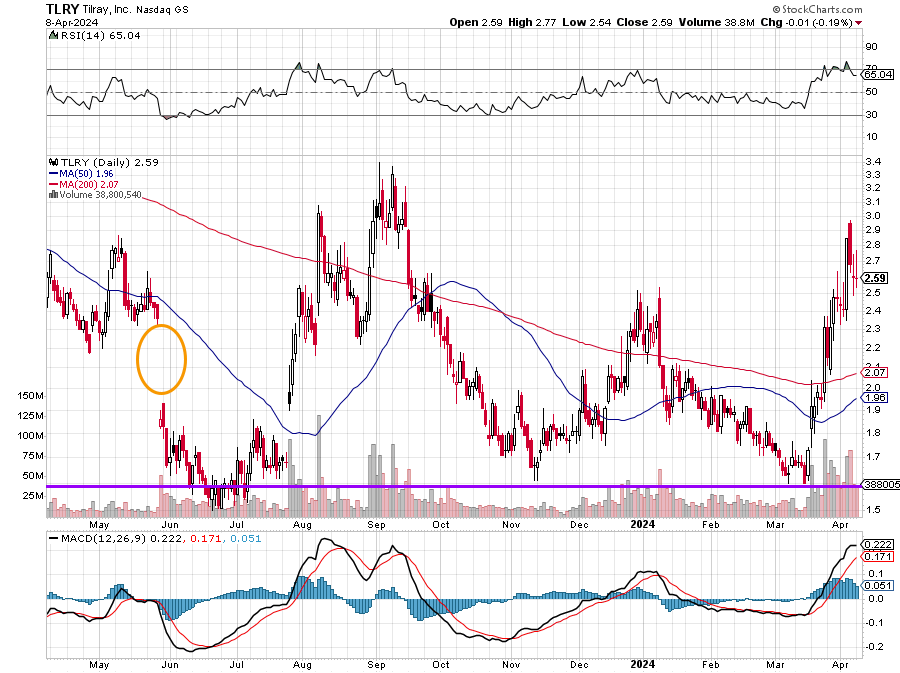

The stock came into these earnings with a strong reading for relative strength and an overextended daily Moving Average Convergence Divergence (MACD). In short, TLRY was ripe for a selloff.

I would not want to pay more than something close to the $1.60s for this stock. The September $1.50 puts went out last night at $0.17. I don't know if that's enough of a premium to take on the potential risk. Let's say with the equity trading significantly lower, I might become interested if this premium doubles. Otherwise, I think I'll just take a walk on this one.

At the time of publication, Guilfoyle had no positions in any securities mentioned.